While my primary focus is the Mid-Peninsula, I know many Bay Area professionals look to the East Bay, specifically the rapidly developing markets of Dublin and Livermore, for relative affordability and space. These areas, however, are especially sensitive to fluctuations in the mortgage interest rate environment. Let’s navigate rate hikes and how they can impact your purchasing power.

As we look ahead to 2026, understanding the relationship between future rates and your purchasing power is the single most critical financial preparation step you can take. Even a small hike can dramatically change the size of the loan you qualify for and the price of the home you can afford.

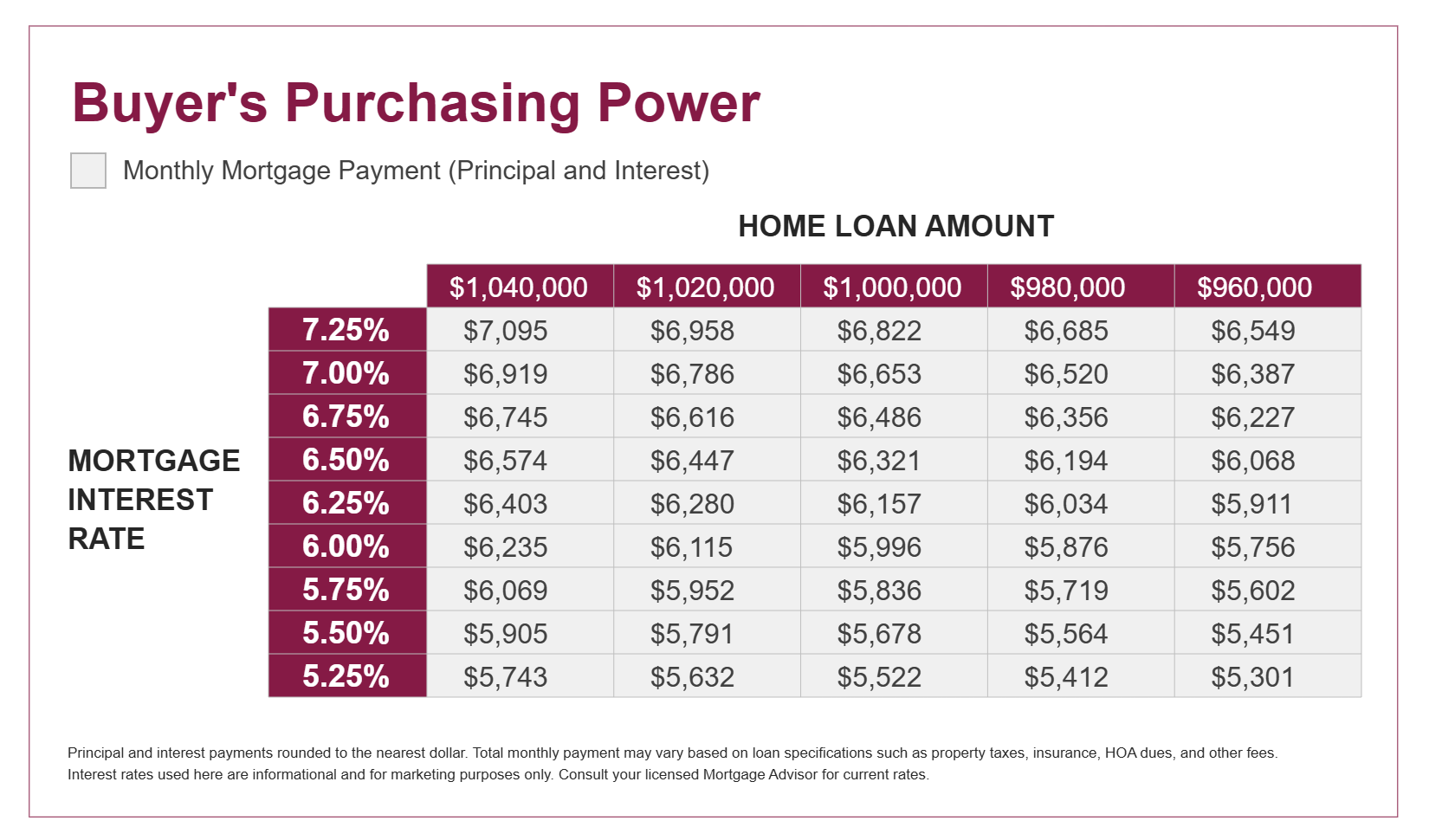

The Math is Simple: Rates and Buying Power

A mortgage loan officer qualifies you for a maximum monthly payment based on your income and your Debt-to-Income (DTI) ratio. If the interest rate rises, a larger portion of that monthly payment is consumed by interest, leaving less room for the principal and thus reducing the size of the loan you can afford.

The general rule of thumb, backed by financial analysis, is sobering: A 1% rise in interest rates can reduce your overall purchasing power by approximately 10%.

📊 Dublin/Livermore: A Rate Hike Scenario

Let’s apply this to a median-priced home in the East Bay, using conservative estimates for Dublin and Livermore (median sold prices around $1.36M and $1.1M, respectively, based on 2025 data).

Assume a buyer is qualified for a maximum Principal & Interest (P&I) payment of $6,000 per month.

| City (Median Price) | Rate 1 (e.g., 6.0%) | Max Loan Amount (Approx.) | Rate 2 (e.g., 7.0%) | Max Loan Amount (Approx.) | Loss in Purchasing Power |

| Dublin ($1.36M) | 6.0% | $1,000,000 | 7.0% | $900,000 | $100,000 |

| Livermore ($1.10M) | 6.0% | $1,000,000 | 7.0% | $900,000 | $100,000 |

Calculations based on a 30-year fixed loan, excluding taxes and insurance (PITI), to illustrate the direct impact of the rate.

The Takeaway: If rates shift by just one point, you could lose the ability to afford $100,000 worth of home. In competitive East Bay markets, that could mean the difference between a 4-bedroom house in a top-rated school district and a smaller 3-bedroom unit further out.

🛑 Rate Volatility Is A Call To Action

What should buyers targeting Dublin or Livermore do right now to mitigate the risk of future rate hikes?

- Marry the House, Date the Rate: Don’t delay your search waiting for rates to fall back to the 3-4% range; those days are likely behind us. Instead, buy the right house now, and plan to refinance later if rates drop. The risk of waiting is that prices continue to climb, negating any future rate savings.

- Save for a Larger Down Payment: A larger down payment directly reduces the loan amount needed, effectively shielding you from the impact of higher interest rates. Aiming for 20% is ideal to avoid Private Mortgage Insurance (PMI) and gain better loan terms.

- Optimize Your DTI: As discussed in my previous posts, ruthlessly pay down credit card debt, car loans, and personal loans. Lowering your Debt-to-Income (DTI) ratio gives the lender more flexibility when calculating your maximum affordable mortgage payment, helping you qualify for a larger loan even at a higher rate.

- Lock Strategically: Once you are in escrow, work with a skilled, local lender to strategically lock your rate. In a volatile environment, a professional can advise you on whether to pay for a longer lock or float your rate based on short-term forecasts.

The Bottom Line for East Bay Buyers

The Dublin and Livermore markets offer incredible lifestyle and community value, but their affordability is fragile. Future rate increases, even minor ones, translate into a serious reduction in your purchasing power.

The winning strategy in 2026 is to secure your pre-approval now, lock in the best rate you can get, and be prepared to move quickly when the right property arrives.

Ready to calculate your current, true purchasing power in the East Bay?

Let’s run a custom P&I analysis that stress-tests your budget against potential 2026 interest rate scenarios.